Portfolio update: Adding a best-in-class E&S insurer

Hi there,

You can track my investment activity through these portfolio updates. I will share my trade details and provide the necessary context around each decision.

I primarily focus on quality businesses. I layed out my investment approach in the very first article I wrote on Substack. You can find it here:

Over the time this portfolio will be available to paying subscribers only, but for now I am more than happy to share the developments.

Please mind: I am investing my own money. Do your own research. This article is not investment advice. Just me sharing my investment journey with my readers.

The short case for Kinsale Capital

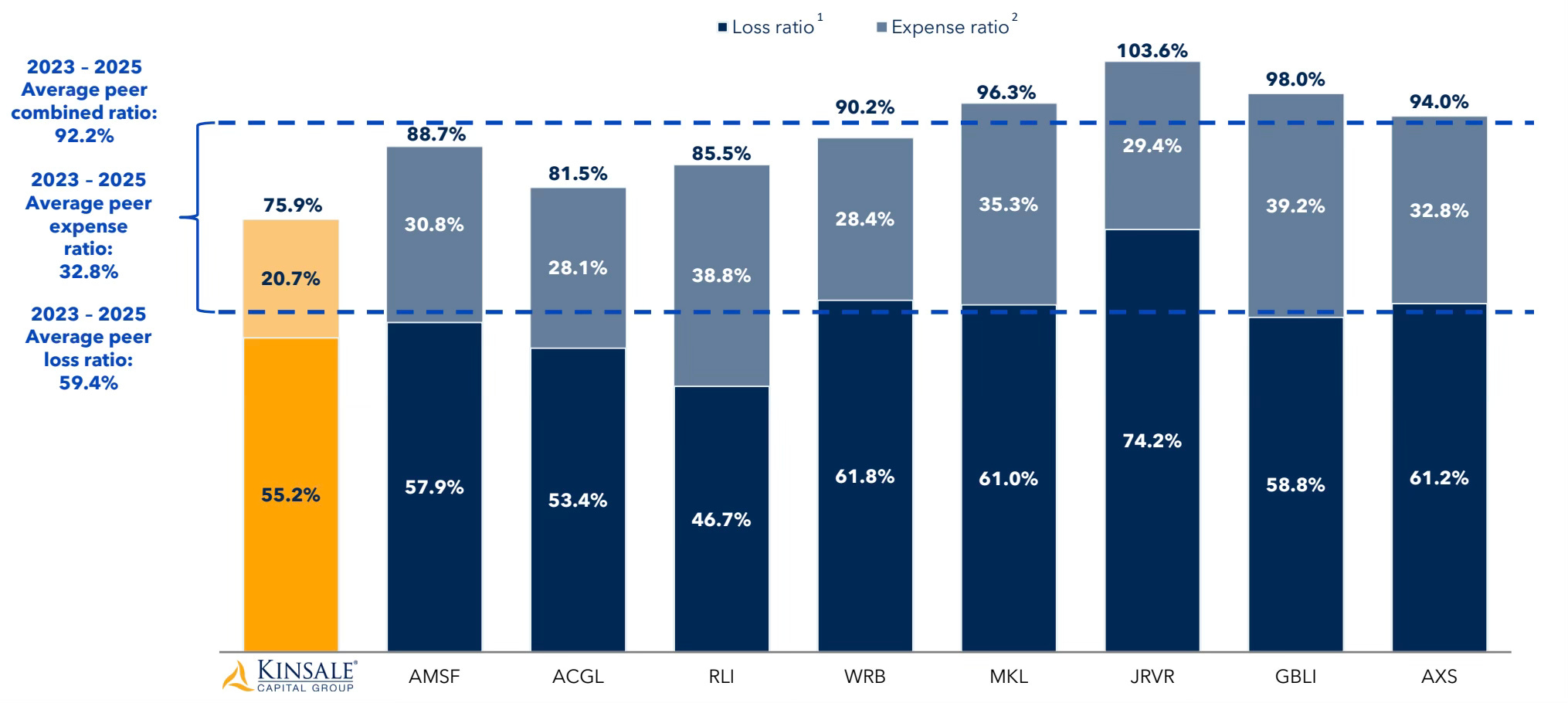

Readers may have noticed that I’m a fan of Kinsale Capital. As a provider of E&S insurance, the company stands out as a best-in-class underwriter, boasting a combined ratio so strong that it leaves competitors far behind.

Kinsale Capital is founder-led by Michael Kehoe, a CEO who exemplifies discipline every time he speaks on an earnings call.

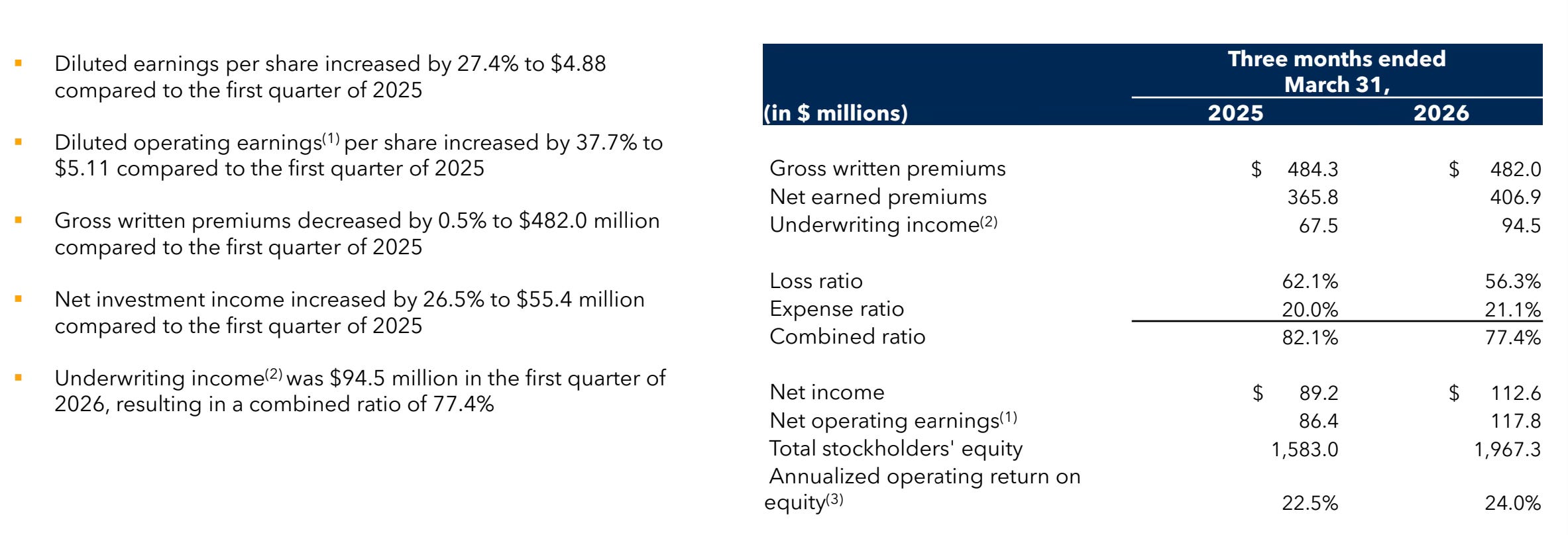

Just last week, the company reported its Q1 results. Gross written premiums edged down slightly (0.5% YoY), reflecting a softer insurance market in its commercial property segment.

Management, however, remained firm in its approach, refusing to bend to Wall Street pressure and staying committed to its “profitability first” philosophy.

The strategy paid off: net income rose 27.4% YoY, supported in part by earnings generated from its steadily growing float.

One final point worth highlighting on the business is Kinsale Capital’s advantage through its technology stack. Unlike many competitors, the company built its platform in-house, which gives it a meaningful edge on costs. No dozens of systems, no migrations needed.

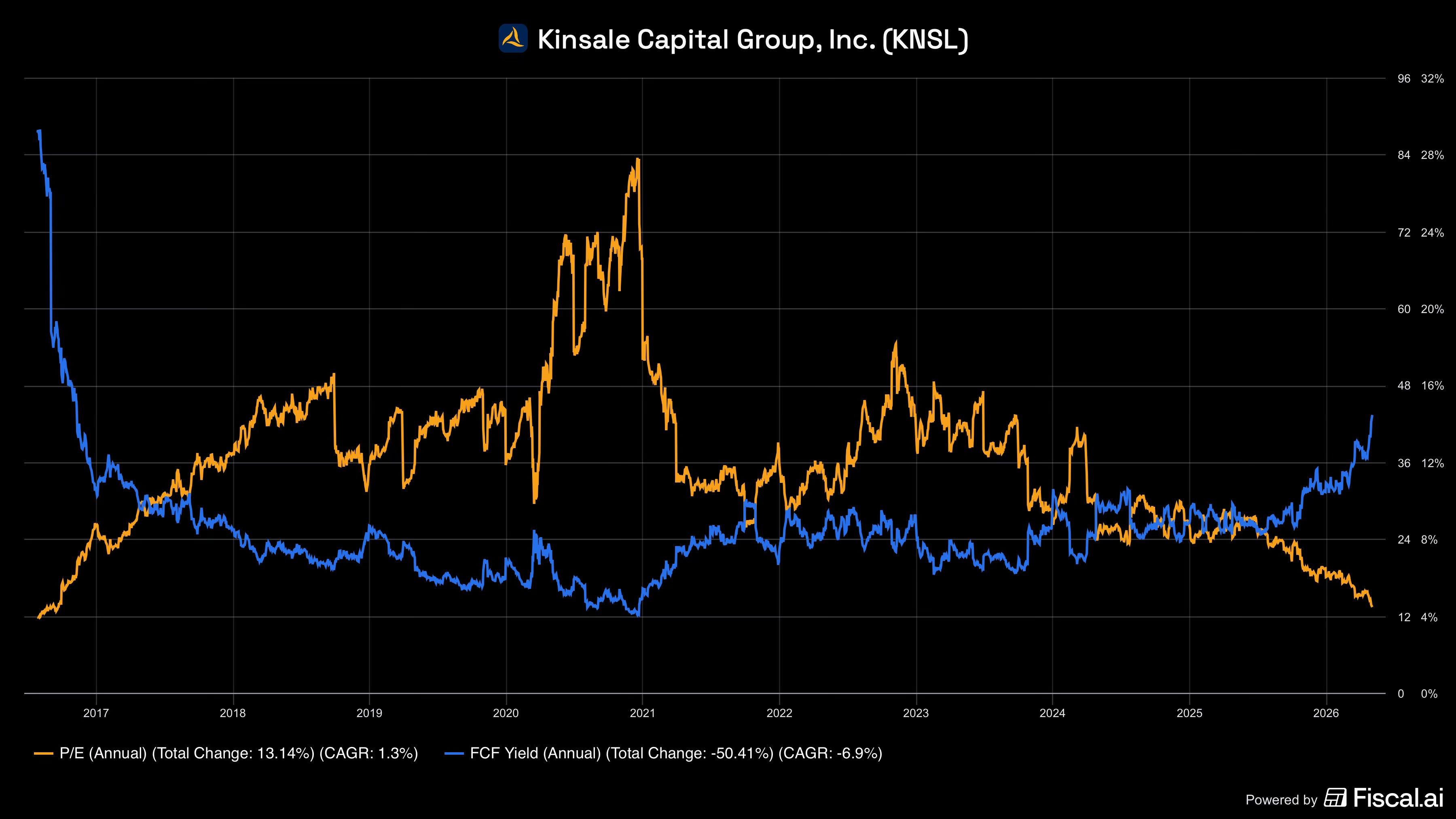

At current levels, I view the stock as undervalued based on a forward P/E of 17.2 and free cash flow yield of 14.4%. The softness in the market is weighing on sentiment, but this phase of the cycle is temporary and will eventually turn for the better.

When the hard market arrives, Kinsale will be perfectly positioned to push rates higher and unleash their underwriting discipline where it matters most, accelerating earnings growth precisely when competitors are retreating. Until then, a growing float keeps compounding quietly in the background, generating strong net income quarter after quarter.

I haven’t published a full deep dive on Kinsale Capital yet, but I’ve been following the business for over a year and have developed a strong understanding of how it operates. That’s why I am comfortable investing.

Trade details

I initiated a position in Kinsale Capital at $305.70 per share. Going forward, I expect gross written premiums to decline further, albeit moderate as Kinsale serves many niches with each undergoing their own business cycle.

This is simply the nature of the insurance cycle. Markets alternate between hard and soft phases, and we are currently in a soft market, which can persist for some time.

That said, I believe Kinsale Capital is well positioned to navigate this environment. Management remains disciplined and consistent in its underwriting approach, which reinforces my conviction. The priority is clear: profitability first, growth second.